A Jerusalem family that lost relatives in a 1997 Hamas suicide bombing is among the plaintiffs pushing a US federal court to order Tether to hand over hundreds of millions in frozen digital currency.

The case, filed in Manhattan, could set a significant legal precedent for how courts treat centralized stablecoin issuers.

A Decades-Old Debt

The plaintiffs are survivors and family members of victims from Iran-linked terrorist attacks. They hold court judgments against Iran that were awarded years ago — judgments that have never been paid.

Now they are targeting a pile of frozen cryptocurrency as a way to collect what they are owed.

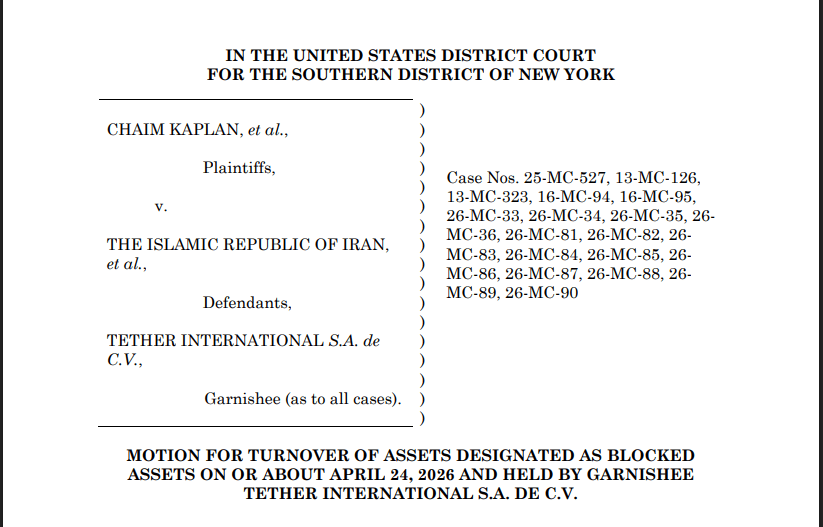

Attorney Charles Gerstein filed the lawsuit Thursday in the US District Court for the Southern District of New York.

Filing against Tether submitted by Attorney Charles Gerstein.

His clients say they have a legal claim to two Tron blockchain wallet addresses holding roughly 344 million USDT. Those wallets were frozen earlier this year by the US Treasury Department’s Office of Foreign Assets Control, which identified them as linked to Iran’s Islamic Revolutionary Guard Corps.

The plaintiffs are not asking Tether to simply release those specific wallets. According to reports, they want a court order directing Tether to transfer an equivalent amount of USDT to their legal team’s wallet address.

Why Tether Can Be Compelled

Unlike Bitcoin or Ethereum, USDT is controlled by a central company. Tether can freeze wallets, block transactions, and move funds when ordered to do so. That centralized structure is at the heart of Gerstein’s legal argument.

Because a prior order already froze the wallets — something only possible because Tether has direct operational control — he contends the company can also be ordered to move the funds.

BTCUSD trading at $78,115 on the 24-hour chart: TradingView

The ownership question, he argues, is already largely settled: OFAC has already declared the wallets to be IRGC-controlled assets, which clears a path for seizure under US terrorism statutes.

Broader Legal Campaign

This is not Gerstein’s only case of this kind. Based on reports, he has filed similar actions involving North Korea-linked cyber operations against the Arbitrum platform. He is also handling a separate case involving Railgun DAO, a privacy-focused crypto protocol.

The Manhattan filing is part of what appears to be a coordinated legal push to test whether courts can compel crypto platforms with centralized control to act on frozen assets held in sanctioned wallets.

Featured image from CEPA, chart from TradingView